Is Salesforce AELA the New SELA?

Salesforce AELA may look like the next SELA, but the risk profile is different. This guide explains how agentic licensing changes pricing, data dependency and renewal leverage for enterprise buyers.

Salesforce has spent two decades training enterprise buyers to think in users, clouds, editions and SKUs. Agentforce changes the commercial centre of gravity. The question is no longer only, “How many people need access?” It is also, “How much autonomous work will run through the Salesforce ecosystem?”

That shift matters because the old licence architecture was built around humans. Sales reps, service agents, marketers, admins and platform users each carried commercial weight. In an AI operating model, some of that human workflow may be compressed, automated or rerouted through agents.

A Salesforce AELA, short for Agentic Enterprise License Agreement, is Salesforce’s answer to that tension. It appears designed to give large customers broad access to Agentforce, Data Cloud and related platform capabilities through a large, multi-year enterprise commitment rather than a narrow per-seat or per-conversation purchase.

For CFOs, CIOs and procurement leaders, the issue is not whether Agentforce is useful. It may be. The real issue is whether the commercial structure matches the organisation’s actual AI roadmap, data architecture and renewal leverage.

Complexity is a tax on the unknown. If they can’t convince you, they’ll confuse you. AELA is exactly the kind of structure where buyers need to separate architecture from enthusiasm, and roadmap from revenue protection.

What Is a Salesforce AELA?

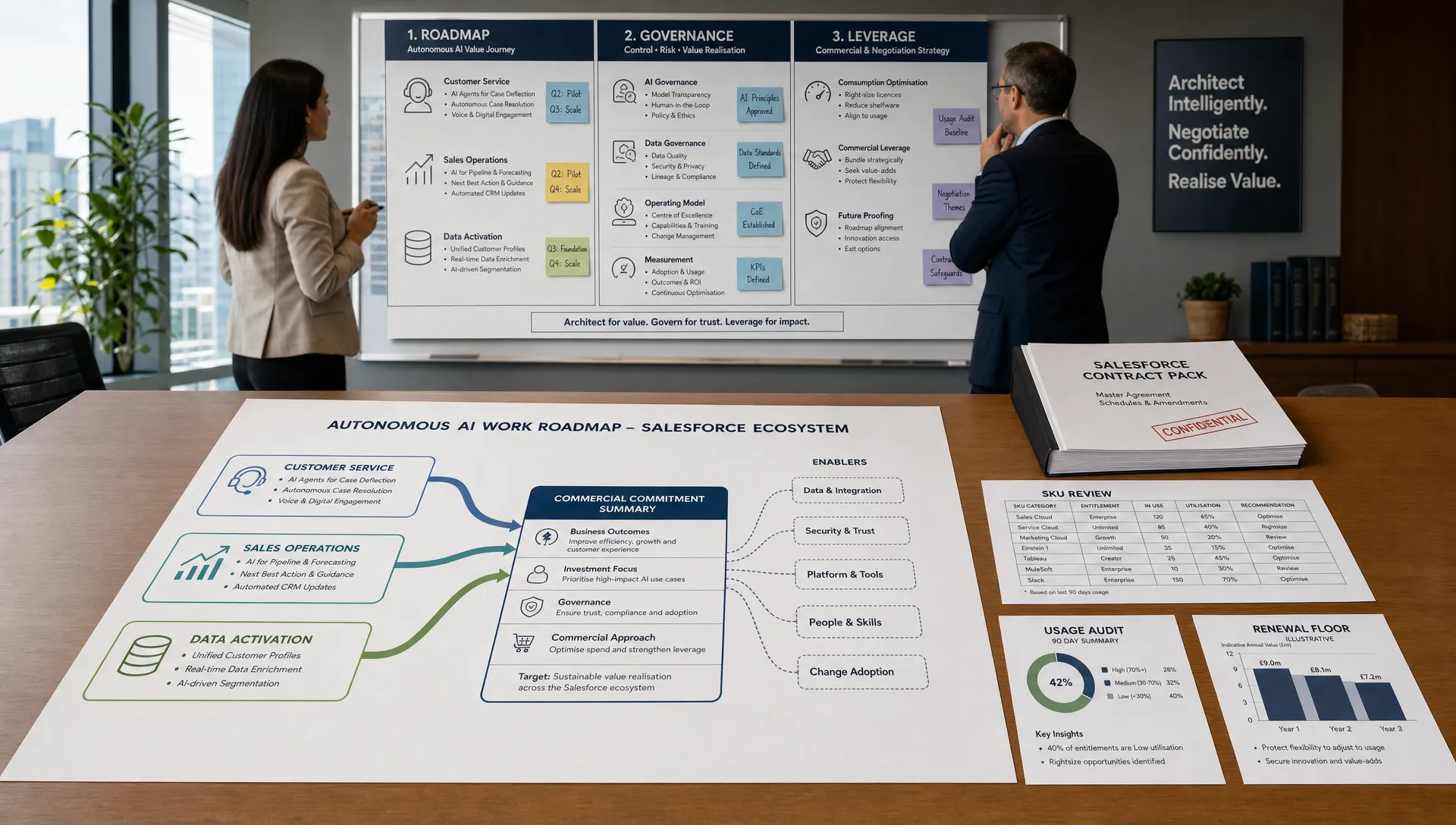

Direct answer: A Salesforce AELA is an enterprise-wide commercial agreement designed to support broad deployment of autonomous AI agents, Data Cloud infrastructure and foundational Salesforce ecosystem integration for a negotiated flat commitment. Unlike standard consumption models, where organisations pay against agent conversations or related usage units, AELA shifts the buyer into a larger upfront framework built around platform-wide AI capacity.

AELA is best understood as a commercial architecture, not a public price list. Terms will vary by customer, estate size, products in scope, region, timing and the level of executive sponsorship inside the account.

Salesforce’s public positioning around Agentforce as a platform for autonomous AI agents gives useful context. Agentforce is not merely another feature bolted onto Sales Cloud or Service Cloud. It is a new layer intended to perform work across customer-facing and operational processes.

That creates a pricing problem. If AI agents resolve service cases, qualify leads, draft responses, update records and orchestrate workflows, then the old seat-count logic becomes less reliable as a revenue base. AELA answers that problem by commercialising the capacity of the AI-enabled platform rather than only the number of human users sitting in front of it.

How is AELA different from per-conversation Agentforce pricing?

In a metered model, the buyer pays as usage grows. That can be attractive when adoption is uncertain because the commercial exposure stays closer to real activity.

In an AELA model, the buyer usually accepts a larger committed baseline in return for broader deployment rights, simplified internal charging and fewer visible adoption brakes. The trade-off is simple: you reduce friction for internal teams, but you may also move spend ahead of proven demand.

That is not automatically bad. For an enterprise with a mature Salesforce estate, governed data foundations and a credible 24-month AI roadmap, it may be sensible. For a company still testing use cases, cleaning data and debating operating ownership, it can become an expensive forecast disguised as a strategic platform decision.

Is AELA the New SELA?

Direct answer: AELA is the successor to SELA in commercial ambition, but not in commercial mechanics. SELA bundled users and products across the Salesforce estate, while AELA shifts the baseline towards agentic capability, data activation and enterprise-wide AI capacity.

A traditional Salesforce SELA, or Salesforce Enterprise Licence Agreement, was built around scale. It bundled large populations of users, multiple clouds and often a negotiated set of products such as Sales Cloud, Service Cloud, Platform, Slack, Tableau or MuleSoft. The commercial conversation was still anchored in human access, even when the bundle became complex.

AELA changes the anchor. It does not simply ask, “How many users will need Salesforce?” It asks, “How much of your operating model will run on Salesforce agents, Salesforce data and Salesforce orchestration?”

That distinction is not cosmetic. It changes what the buyer is really buying.

With SELA, the hidden risk was often shelfware. You might commit to more licences, editions or adjacent products than the organisation could absorb. With AELA, the hidden risk is architectural dependency. You may commit to a future operating model before your business has proved that it wants that model, can govern it, or should source it entirely from Salesforce.

For readers who want the broader commercial context, SaaSed has already mapped the wider shift in Salesforce commercial structures from standard agreements to SELA and AELA. This article goes deeper into the architectural procurement consequences of AELA specifically.

Why would Salesforce move from seats to agents?

The seat model is exposed when automation becomes credible. If AI can handle work that previously required incremental human licences, seat growth becomes a weaker predictor of vendor revenue.

AELA gives Salesforce a way to protect and expand enterprise spend even if employee licence demand flattens. It reframes the value baseline from “number of users” to “amount of work the Salesforce platform can automate”.

This is why buyers should look past the surface narrative. The vendor may describe AELA as simplification. Procurement should also recognise it as revenue continuity.

Neither interpretation is unfair. Both can be true at the same time.

AELA vs. SELA: What Is the Difference?

Direct answer: SELA is mainly a licence consolidation structure for human users and legacy Salesforce product SKUs. AELA is an AI-era platform commitment that blends agent deployment, data infrastructure and ecosystem dependency into a larger commercial frame.

The structural evolution is easiest to see through the pricing metric. SELA made large estates easier to package by turning many individual licences into an enterprise construct. AELA goes further by attempting to commercialise the future work capacity of AI agents.

That makes the negotiation harder. In a SELA negotiation, the buyer can usually test the proposal against known inputs: deployed users, inactive users, product adoption, contracted SKUs, ramp schedules and business unit demand.

In an AELA negotiation, many inputs are probabilistic. The buyer must estimate future agent volume, use case maturity, data readiness, workflow redesign, business adoption, compliance controls, AI governance and the likelihood that Salesforce will remain the preferred AI execution layer.

That is a much more speculative deal model.

How does AELA solve Salesforce’s AI monetisation problem?

AI creates a paradox for enterprise SaaS vendors. If AI increases productivity, buyers may need fewer seats. If fewer seats are needed, traditional subscription growth becomes harder.

AELA resolves that paradox by charging for AI-enabled capacity and ecosystem commitment rather than relying solely on headcount-linked access. In practical terms, it protects Salesforce’s commercial floor while giving the customer permission to scale agentic workflows without negotiating every incremental use case.

The buyer should not object to Salesforce monetising value. Vendors are entitled to be paid for meaningful capability. The procurement concern is whether the payment structure reflects value actually captured by the customer, or value the customer is merely expected to capture later.

What Are the Strategic Traps of the AELA Structure?

Direct answer: The main risks of AELA are not only price, but dependency, internal option loss and renewal-floor expansion. The agreement can look efficient in year one while quietly narrowing the buyer’s future sourcing choices.

AELA creates a particular kind of procurement problem because the commercial logic is attractive. If a flat enterprise fee makes Agentforce feel “already paid for”, internal teams may naturally default to it for AI use cases. That can be useful where standardisation is the goal. It can also crowd out better-fit tools before they receive a fair evaluation.

The following risks deserve board-level visibility before signing.

- Integration Gravity: A flat, broad AELA fee can create an internal Salesforce AI monopoly. Once business units are told that Agentforce is covered under the enterprise deal, procurement may find it hard to approve specialist AI tools later, even when those tools are better suited to a particular workflow.

- Data Dependency Lock-in: AELA will often increase reliance on Salesforce Data Cloud or adjacent data services as the context layer for agents. Salesforce describes Data Cloud as a way to unify and activate customer data, which may be valuable, but deeper data centrality also raises future switching costs.

- The Baseline Floor Mirage: “Unlimited” can sound like the removal of constraints, but enterprise agreements often carry minimum commitments, scope assumptions, architectural dependencies and renewal baselines. At the three-year renewal, the starting point may be the AELA floor, not actual realised value.

- The Forecasting Gap: Agentic usage is hard to forecast because most organisations do not yet know which AI use cases will survive compliance, adoption and operational scrutiny. If the AELA is priced on optimistic use-case volume, the buyer carries the risk of under-adoption.

- The Governance Drag: Autonomous agents touch data quality, security, permissions, auditability, customer experience and operational controls. If those governance layers are immature, broad commercial access may accelerate experimentation faster than the organisation can safely govern it.

The critical point is not that these risks make AELA unsuitable. They mean AELA needs to be evaluated as architecture, not as a discount vehicle.

A useful parallel comes from brand and market positioning. Strong challengers do not buy a category narrative just because the incumbent names it well; they test whether the narrative serves their own growth plan. That same discipline applies here, and it is why challenger go-to-market thinking is relevant even in a software procurement room.